HOW MY CREDIT SCORE AFFECTS MY AUTO LOAN

Car shoppers with low credit scores often visit multiple car lots trying to learn how their credit score will affect purchasing a new car. Though the process may seem complex, understanding your credit score can make it a lot easier. Here’s the breakdown of credit ratings, buying a car with a low score, and how an auto loan can help you rebuild for your future.WHAT IS A CREDIT SCORE?

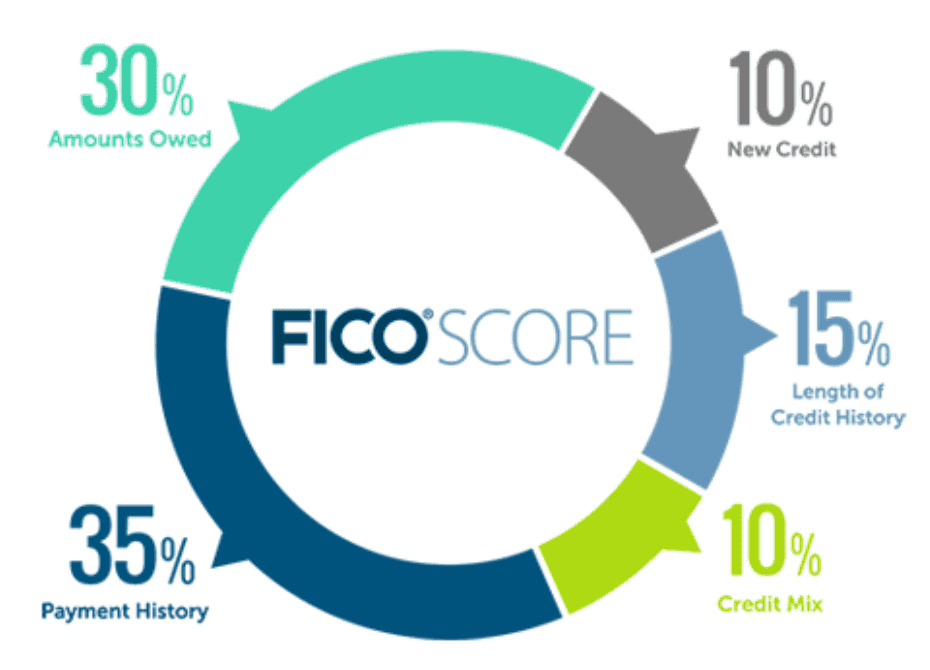

A credit score is a three digit number that represents your credit history. Many credit scoring calculators exist, but the one that you should pay attention tois your FICO score. FICO credit scores range from 300-850. Your credit score dictates the interest you will pay on your auto loan.

HOW BAD CREDIT CAN AFFECT YOUR CAR LOAN

If you score a 700 or higher, you will get the best interest rate on an auto loan. If your score is lower than 580, you could be looking at an interest rate as high as 20 percent. In addition to your credit score, lenders will look at your debt to income ratio, length term of the loan, amount needed, and the age of the vehicle. Check out this article that details the five things lenders use to decide auto loan interest rates.

As you shop for a car, try to avoid ‘buy here pay here’ dealerships, these types of dealerships often do not report to credit agencies, thus your score won’t change even if your loan is paid on time and in full.

HOW YOU CAN REBUILD YOUR CREDIT

If you are trying to improve your credit score, it’s important to note that it’s a process and it takes time. Building your credit is often compared to losing weight: there is no quick fix and it takes consistency and time. There are three things you can do right now to start rebuilding your score:

Check your credit report.

You can request a free copy of your credit report and check it for errors. Your report includes data that is used to calculate your credit score. Check to make sure there are no late payments listed incorrectly, and the amounts owed on each account are updated. If you find any errors, contact the credit bureau and file a dispute.

Reduce your overall debt.

Start a plan that puts most of your available budget towards making payments on the lines of credit with the highest interest rates and then continue the minimum payments on all other accounts. Reducing the amount you owe will be a greater achievement that just increasing your score.

Setup payment reminders.

Most lenders and bank institutions will allow their customers to set up automatic payments with email or text message reminders each month. Making your payments on time is one of the biggest contributing factors to your overall credit score.

SUMMARY

Your credit score matters. Your credit history defines your score, but you have control over your credit future. Keeping a score over 700 will ensure you get the best interest rates on loans. If you want to rebuild your credit score, start by checking your credit report and putting as much of your available budget to paying off your debt. Getting an auto loan and making your payments on-time will show consistency and responsibility and will improve your score over time. Having a solid grasp on your credit situation will help you be self-assured and prepared when making the smartest car purchase.